- unhashed

- Posts

- Sid Powell and Maple Finance: $20 Billion Later, DeFi Is Dead. And That Is the Point.

Sid Powell and Maple Finance: $20 Billion Later, DeFi Is Dead. And That Is the Point.

How a former securitization banker built one of the largest on-chain credit businesses in the world by betting that DeFi's original identity was its biggest liability.

The suits were a tell. At Digital Asset Summit in New York earlier this year, the crowd that once wore hoodies to conferences was, by and large, in blazers. Sid Powell, co-founder of Maple Finance, was among them, and he did not seem uncomfortable. He spent years structuring securitizations in traditional finance before deciding that smart contracts could do the same job faster, cheaper, and without the Monday-to-Friday settlement window. The suits, he will tell you, are not a concession. They are a conquest.

"No plan survives first contact with the enemy. We started with the idea of tokenizing bonds, but there were no bonds to tokenize and no investors on-chain for that. So we had to pivot to direct lending."

That willingness to keep pivoting is the story of Maple. From tokenized bonds to uncollateralized lending, through the damage of 2022, then to over-collateralized lending, and now toward fintech asset-backed facilities and loans against tokenized equities. Each time the market got crowded, Sid found the next empty space and moved before anyone else noticed.

What "institutional credit in DeFi" actually means

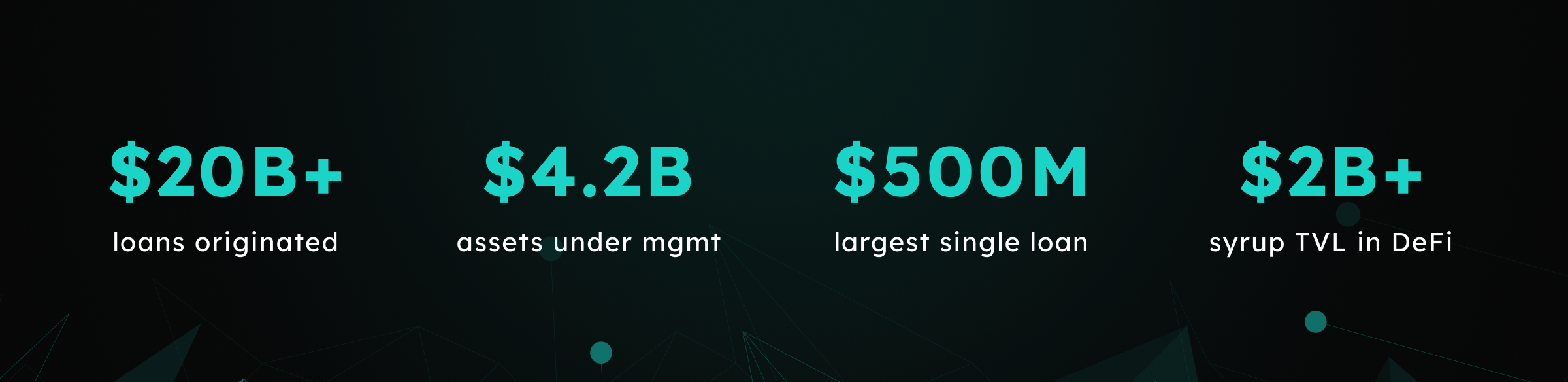

When Sid says institutional credit, he means large ticket sizes, minimum $10 million, to exchanges, prime brokers, and asset managers who post Bitcoin, Ethereum, or Solana as collateral. The product is deliberately designed to feel familiar to borrowers used to TradFi counterparties. No smart contract liquidation. A margin call notification, 24 hours to post, collateral held in qualified tri-party custody. Maple's largest single loan, a $500 million facility, closed just before Christmas 2025.

"It is a tailored product that invites large institutional players to interact more and more with DeFi. And DeFi benefits by getting sustainable yield, not from looping or points farming, but from real commercial activity and credible borrowers."

The mechanics matter. Protocols like Aave liquidate all of a borrower's collateral because they have no relationship and no basis for discretion. Maple liquidates only back to the initial loan-to-value ratio and charges no penalty. Sid makes the incentive structure explicit: DeFi protocols make most of their money when they liquidate borrowers. Maple makes money when borrowers pay interest. In practice, 99 percent of Sid's margin call cases are resolved within two to three hours.

2022, the rebuild, and a better ratio

It would be dishonest to discuss Maple without discussing 2022. When Three Arrows, Celsius, and FTX collapsed, the uncollateralized lending market went with them, and Maple was not immune. The lesson Sid took away was structural, not technical.

"There is no real technology moat. All you can do is execute faster than your competitors. We were infrastructure in 2021, and in infrastructure you lose too much margin. Vertical integration has been the biggest lesson."

Since 2023, Maple has written its own smart contracts, curated its own vaults, and managed the full credit process end to end. The numbers show what that discipline produces. In 2022, Sid had roughly 40 people managing $1 billion in assets. Today, still 41 people, the platform manages $4.2 billion. Four times the capital, roughly the same headcount. Sid credits automation and AI-assisted workflows for that ratio.

The next wedge, and where it leads

Bitcoin-backed lending has a ceiling set by the total market cap of digital assets held by willing institutional borrowers. Sid knows this, and he is already moving. The direction is fintech asset-backed lending: card issuers, invoice finance lenders, small and medium business lenders, none of whom have historically had any reason to engage with stablecoins. They are interested now because the cost of on-chain capital has fallen far enough to make Maple competitive with traditional private credit funds and banks.

"For the first time, we can go out as a crypto lender and quote a facility of $100 or $200 million. This is where we start to eat TradFi's market share."

The structure Sid has in mind is standard securitisation: an SPV holds the rights to cash flows, whether card receivables, auto loans, or invoices, and Maple funds a senior position. Duration stays under 12 months, investment grade only. This is not the software-company private credit attracting concern in traditional finance. Sid is careful to draw that line. Private credit is a $3 trillion market with many subsectors. He wants the senior, asset-backed, short-duration corner of it.

Sid is also already receiving pitches for loans against tokenized Nvidia shares and Mag-7 stocks. His logic is direct: Nvidia's market cap is comparable to Bitcoin's. If Maple lends against Bitcoin, there is no principled objection to tokenized Nvidia. He believes Maple could be accepting collateral across three to five tokenized asset markets in multiple jurisdictions by end of 2027. Over the past two weeks alone, he has fielded pitches from Hong Kong, Singapore, London, and Dubai.

The Syrup products sit behind all of this as the capital intake mechanism. Syrup USDC and Syrup USDT have each crossed $1 billion, giving Maple more than $2 billion in DeFi TVL. The firm is targeting $100 million in annual recurring revenue by end of 2026, building on a monthly record of $2.49 million set in October 2025. TVL grew nearly ten times in 2024 alone.

Sid's stated ambition is to become one of the largest alternative asset managers in the world, using blockchain the way Amazon used the internet: same business model as Apollo or Blackstone, different technology stack, and a compounding advantage the incumbents cannot replicate without dismantling 30 years of operational infrastructure. That is not a modest goal. But then, neither was lending $500 million in a single transaction from a 41-person team running on stablecoins.

The DeFi that Sid declared dead required you to understand yield farming to use it. The one he is building requires a Bloomberg terminal, a custodian relationship, and a legal entity. That is a much larger market, and it turns out the suits were always the plan.